The Bordeaux 2021 En Primeur campaign has been one of the least successful of recent times. Yet again, many buyers and collectors have had to ask what purpose the time-consuming event serves when it delivers such pitiful revenue and who precisely it is for when it offers little compelling value.

In our opening report we suggested this was another vintage that could be used to energise the en primeur market. Not one of the great vintages but one with potential, that could be offered at accessible prices. However, this was not what the 2021s delivered.

Comparing sales of the 2021s to the 2020s, feedback from merchants across the globe is that most sold far less than last year, with volume and value sales down by as much as 60% in a few cases. In some instances, sales of usually bankable wines crashed to almost zero.

Although 2021 was a small vintage with quantities of dry and sweet wines particularly badly affected, the châteaux policy of reducing the volume of stock released to market continued.

The pace of the campaign was also irregular, broken up by trade fairs and bank holidays. Merchants occasionally found themselves scrambling to focus with an increasingly high tempo of releases as the campaign went on, not helped by some estates releasing when they weren’t expected. It also seemed that little consideration was given to the wider macroeconomic conditions and the impact this would have on buying appetites.

According to one member, the result was ‘predictable chaos’.

Merchants, journalists and critics walked away from the spring tastings having realised the 2021s were not as weak as feared. ‘All the conditions were there to have a good campaign,’ said one Liv-ex member. The problem was that too few wines offered relative value.

The overall trend of the campaign was estates releasing their 2021s at the same price as the 2020s. On average, the 2021s were scored two-points lower than the 2020s by Neal Martin (92-points versus 94-points) yet the average release prices of the 2021s were less than 1% what the 2020s had been – and many 2020 wines remain available at their release price.

That being said, there were some reductions. For example, Château Léoville Las Cases delivered the biggest price drop of 14.6% compared to last year’s release (although this still looked poor relative value).

Some wines also raised their prices. Clos du Marquis – also from the Domaines Delon stable – had the biggest price rise among the red wines, up 12.9%. Most of the big increases though came from the white wines, with producers counting on tiny volumes and high critical acclaim to drive demand.

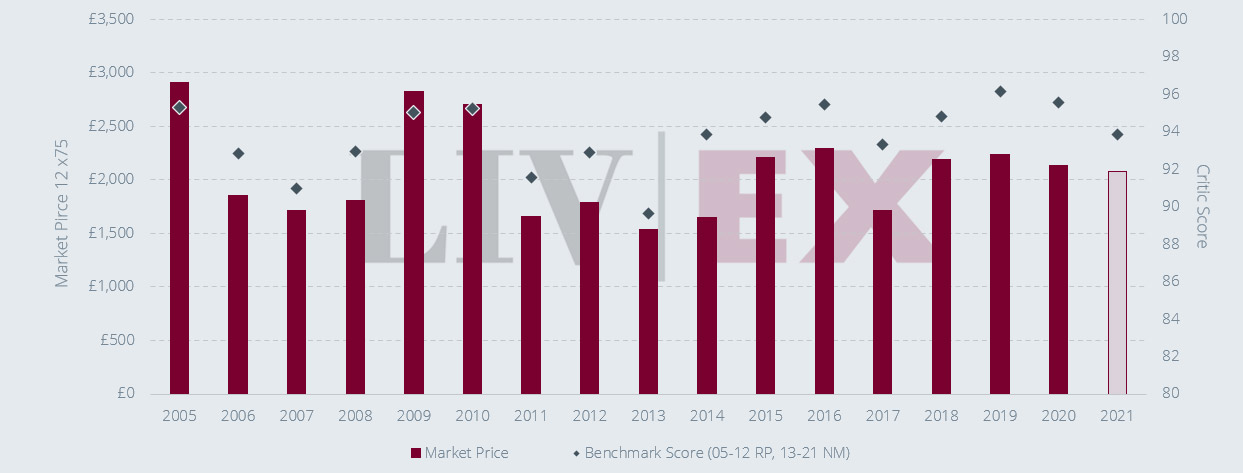

The chart below shows a comparison of the average scores and Market Prices of wines in the Bordeaux 500 index.

Source:www.liv-ex.com

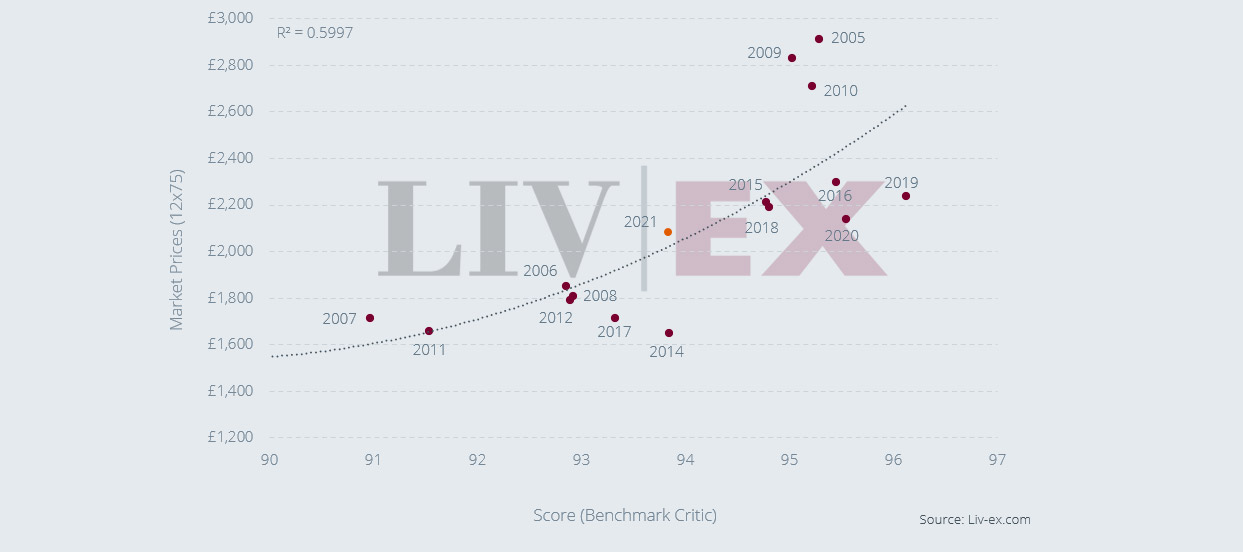

Using the Liv-ex Fair Value methodology, the position of the 2021s in the market versus previous vintages becomes even more stark.

Source:www.liv-ex.com

In terms of average score, it is better to compare the 2021 vintage with 2014 rather than 2020. Yet the 2021s were priced in line with the 2020 vintage. With the average Market Price of the 2014s being 1.918 Euro per case (12x75) – 20% lower than the average release price of the 2021s (2.424 Euro) – many found better opportunities in back vintages.

Even broadening the selection to wines not in the Bordeaux 500, on average the 2021s are 17.9% more expensive than the current Market Price of the 2014s and 15% more expensive than the 2017s.

The successes of the campaign were few but some wines did sell. The First Growths (some second labels too), Lafleur, Calon Ségur, Les Carmes Haut-Brion and Cheval Blanc were all names mentioned frequently in feedback from merchants.

Cheval Blanc in particular has gone from being ‘a hard sell to the darling of the campaign,’ said one respondent.

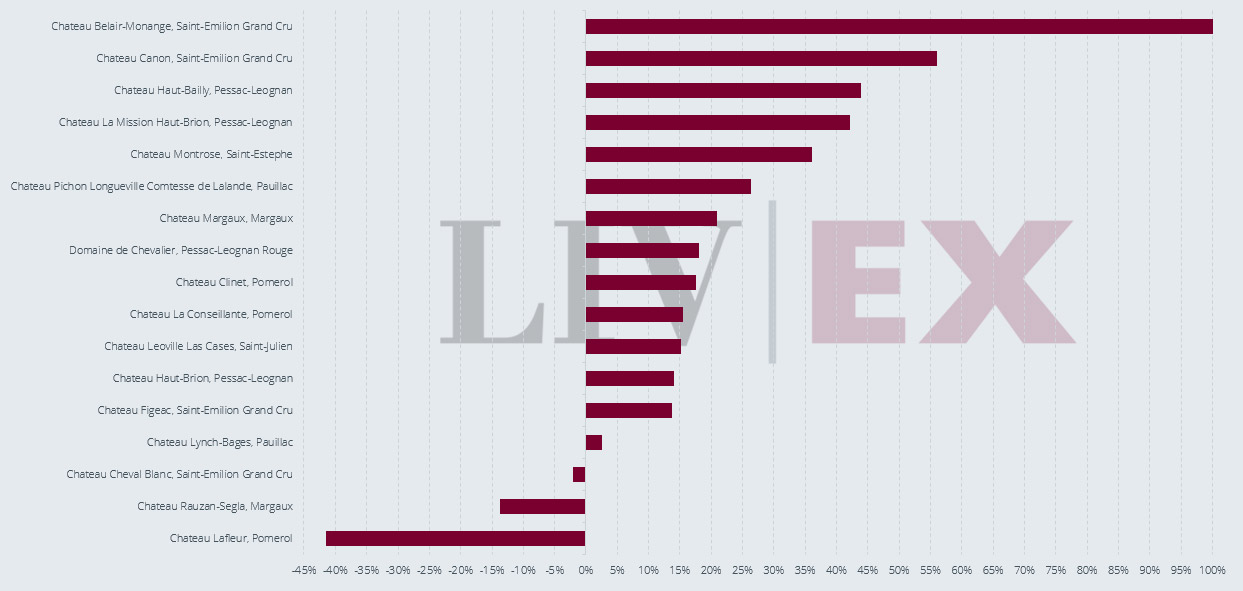

Most (though not all) of the better-selling wines looked good because they offered ‘fair value’. However, as discussed above and as the chart below demonstrates, this was rare.

Source:www.liv-ex.com

But even among the better judged releases there was a gripe – a continued restriction on the amount of stock being released. Most of the releases were down 20%, 30% or even more on the amount released last year.

2021 was a relatively small vintage and some estates lost a large proportion of their crop. For this reason, Château Haut-Bailly’s release was 60% lower than last year. But other estates escaped the frost and mildew problems relatively unscathed and still cut release volumes by 30%.

This withholding of stock from the market has been discussed in numerous reports. Needless to say, it in no way helps merchants who miss out on sales, and it negatively impacts the secondary market performance of Bordeaux, which in turn makes collectors seek opportunities elsewhere.

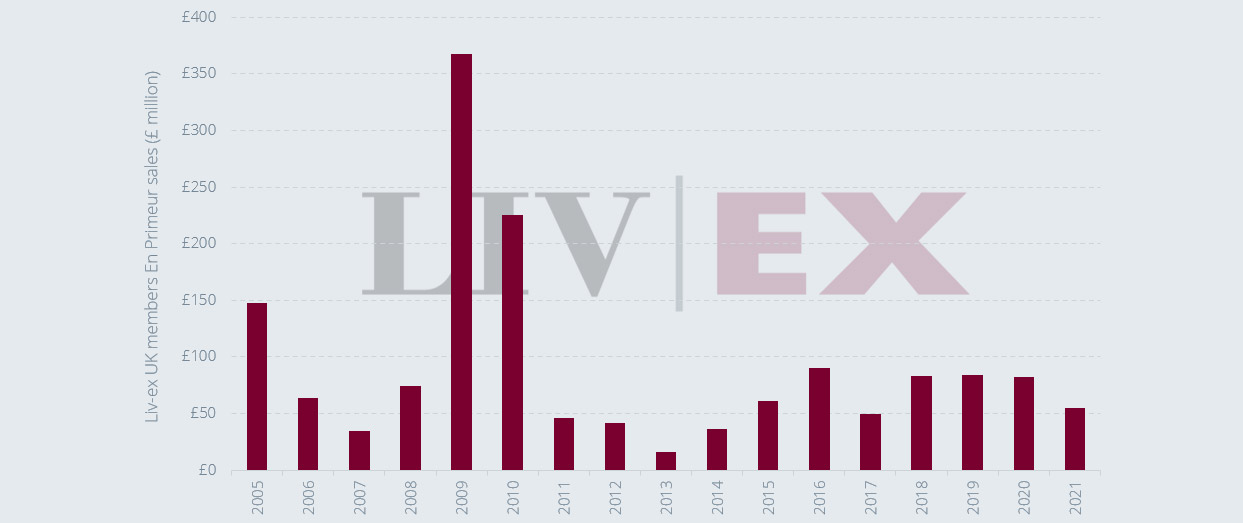

As a result, when looking at the sales of UK members (the largest single country buyers of EP) , it’s clear this has been a weak campaign. The final sales tally is just stronger than 2017 but it flatters to deceive. The anecdotal reports from merchants suggests this was a campaign with a greater emphasis on preserving allocations of the top wines (by and large released more expensively than in 2017), while fewer wines sold through overall, if at all.

Source:www.liv-ex.com

The 2021 campaign has done little to address the identity crisis of En Primeur – indeed it has likely worsened it. This is a vintage that was destined for the dining tables, not decades in cellars. Now it is destined for discounts. Even before the end of the campaign, offers were appearing on the market up to 15% cheaper than their opening price. It would not be surprising to see higher discounts over the coming months and years.

The region’s producers cannot continue to offer middle-of-the-road vintages at prices scarcely distinguishable from those it declares great which then crash in value post-release. Maintaining pricing levels and restricting stock may be regarded as part of a process of preserving brand equity for those on the inside looking out. But for those on the outside looking in, it appears nonsensical, self-defeating and, ultimately, a reason to stay away.

In the same week that the Bordeaux campaign wound up, with releases from Margaux, Mouton, Haut-Brion, Figeac, Calon-Ségur, Clos Fourtet and Cos d’Estournel – Burgundy had its highest ever share of weekly trade in the secondary market.

The 2019 campaign demonstrated that there was a willingness to cut prices in a period of great economic uncertainty. The economic circumstances during this campaign were arguably worse and the vintage nowhere near as good yet prices were kept at last year’s elevated level. It is confounding but the results were indeed ... predictable.

This article was originally published on Liv-ex, the global marketplace for the wine trade. Data within it reflects the independent, real-time buying and selling activity between hundreds of the world's most active and most reputable wine businesses. Discover the smartest way to price, buy and sell wine!